Stock owners are pulling away from most other Americans

Our exclusive Better-Off Index shows that the stock market is about the only thing going right in the US economy.

One group of Americans is doing great: Those who own stocks.

The rest are living in a different world.

The Pinpoint Press Better-Off Index shows a modest improvement in US living standards compared with one year ago. But it’s largely because of stock-market gains. Without stocks, the year-over-year improvement is much weaker. And on the measures that matter most to working-class Americans, the economy is stagnant and probably getting worse.

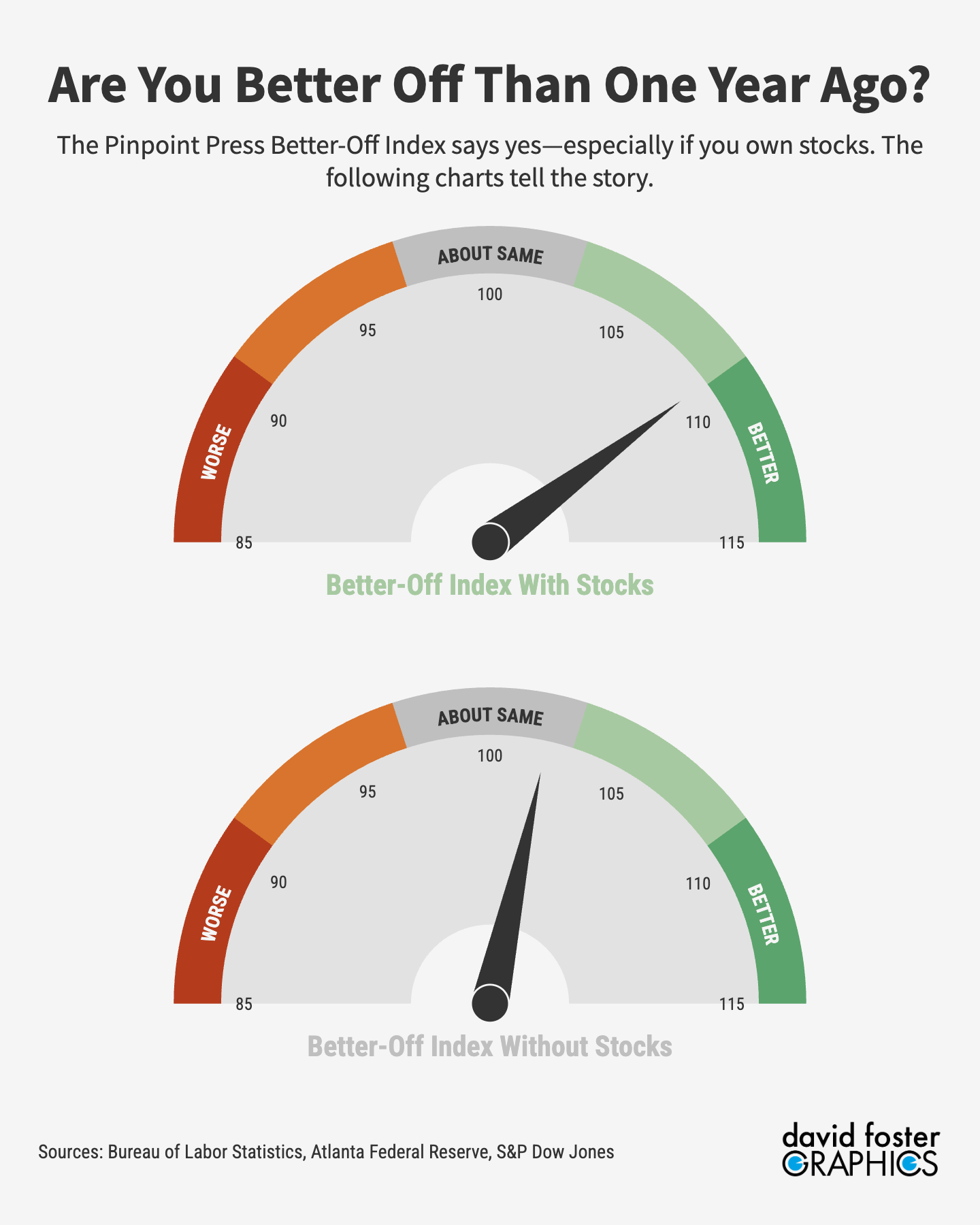

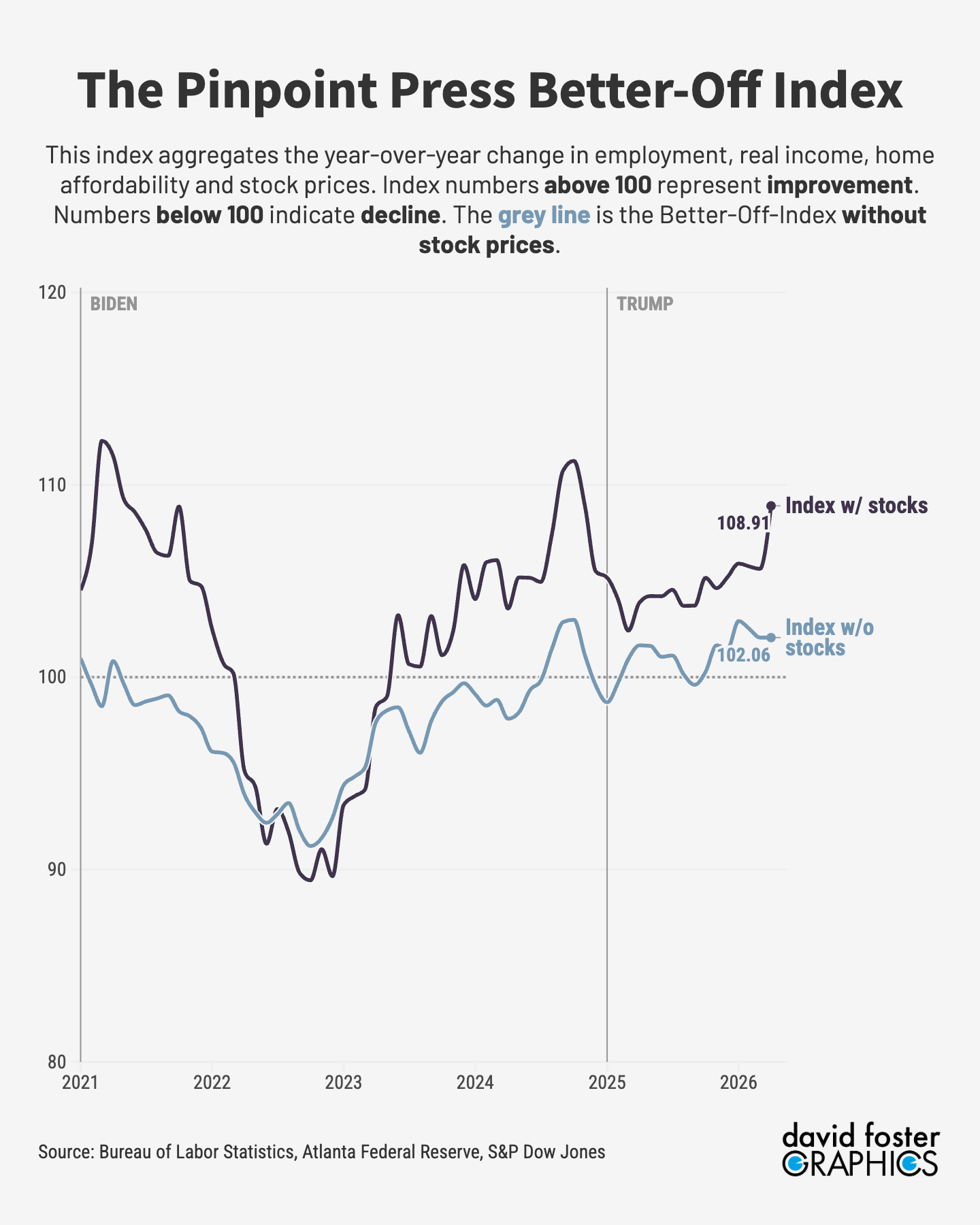

The Better-Off Index answers the question, are we better off than we were one year ago? The index compiles four basic economic metrics—job growth, income growth, home affordability and stock-market performance—into one number, with values over 100 indicating improvement and values below 100 indicating decline.

The Better-Off Index through April is 108.91, which is an 8.9% improvement over conditions one year earlier. That’s up from 105.63 in March.

But without stocks, the Better-Off Index is just 102.1 for April. And most of that was due to improving home affordability. Growth in employment and real income, adjusted for inflation, was extremely weak, revealing substantial stressors for working Americans who aren’t building wealth through home ownership or stock-market investments.

This disparity illustrates the “K-shaped economy,” with Americans who hold financial wealth representing the upper leg of the K, and doing quite well. They’re benefiting from a huge rally in stocks that’s been going on since late 2023, with the S&P 500 index up 76% since then. Upper-K Americans also tend to be homeowners, and the luckiest of those bought before 2021, allowing them to refinance at the record-low mortgage rates that followed the 2020 Covid pandemic.

~ ~ ~ ~ ~ ~ ~ ~ ~

Check out everything The Pinpoint Press offers:

~ ~ ~ ~ ~ ~ ~ ~ ~

Lower-K Americans are typically workers who rely on a paycheck alone, with little financial wealth to pad their living standards. While slightly more than half of all Americans own stocks, many of those holdings are in retirement accounts that are generally untouchable for working-age people. And even those holdings tend to be small. The wealthiest 10% of Americans own 87% of all stocks, according to Federal Reserve data. The next 40% own about 12%, while the bottom 50% own just 1% of all stocks.

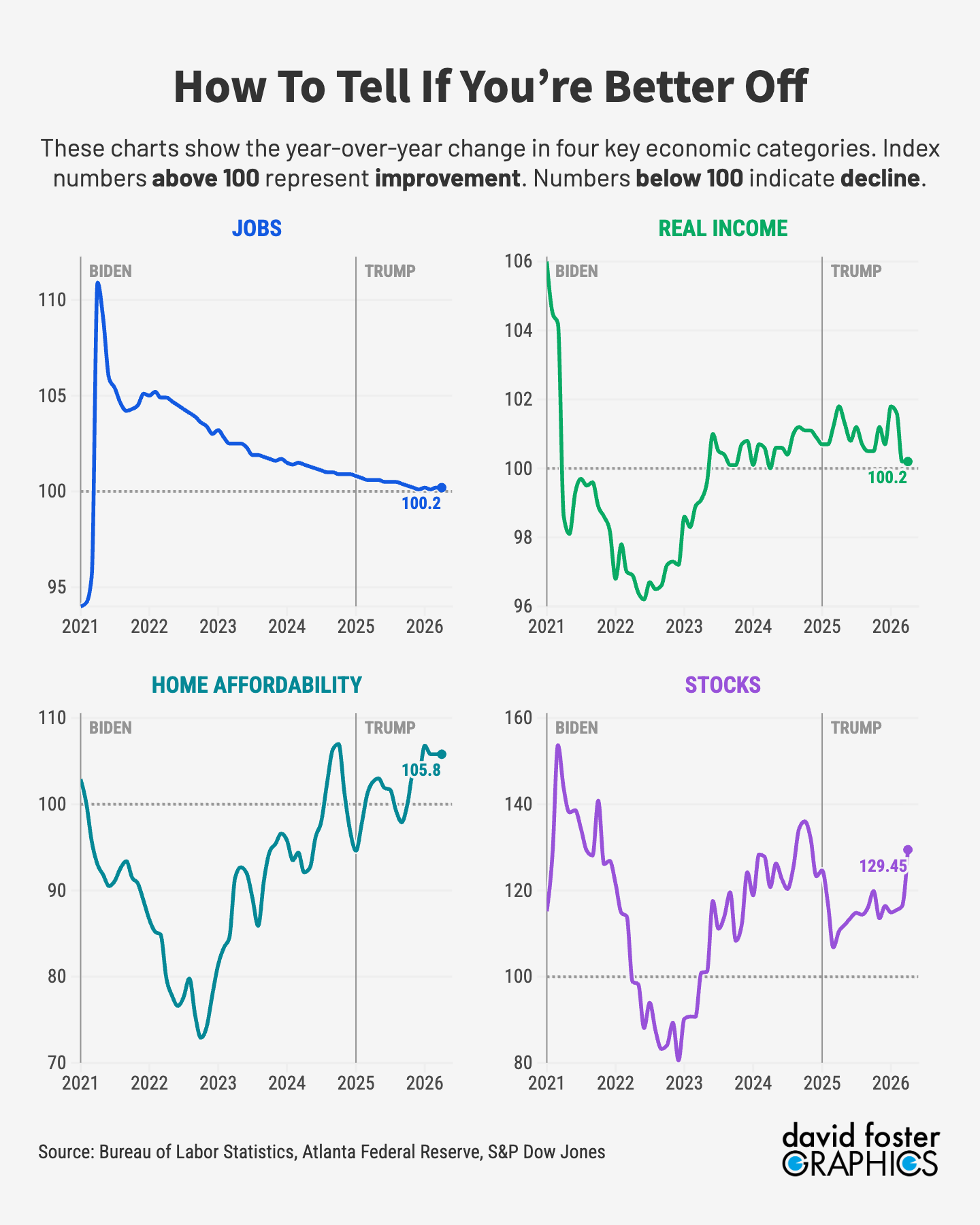

Affordability and inflation are once again top concerns for many Americans. The Better-Off Index accounts for inflation in two ways. The first is real income, which is income adjusted for inflation. As the chart above shows, real incomes were negative for much of Joe Biden’s presidency. That’s because of runaway inflation that peaked at 9% in 2022, which was far higher than nominal income growth.

Real income turned positive late in Biden’s term, and went a bit higher when President Trump took office, largely because inflation fell to a low of 2.3%. But inflation is on the march again, due to Trump’s war with Iran and surging energy prices. Inflation is now 3.3% and almost certainly going higher. Real incomes, as a result, are barely higher than one year ago and will probably turn negative soon.

Home affordability also captures inflation, specifically housing inflation. Home affordability is improving on a year-over-year basis, because mortgage rates are lower than they were in 2025 and the growth in home prices has slowed.

But housing affordability remains poor. It takes 41% of median income to pay for a typical house, according to the Atlanta Federal Reserve, which is far higher than the affordability threshold of 30%. Housing costs have been above the 30% threshold since 2021, when low rates led to a surge of buying, pushing home prices up and up.

Housing affordability is also likely to worsen. The latest data is from February—before Trump launched the war against Iran—when the average mortgage rate was 6%. The Iran war has pushed interest rates higher, with the average mortgage rate now around 6.3%. So home affordability will likely worsen in future data.

Many Americans don’t need charts and indexes to know that their paychecks are stretched. Consumer confidence, by some measures, is close to the lowest levels on record. Trump’s approval rating is sinking, especially on economic issues. His net approval rating on the economy has dropped from +12 to -24, according to YouGov. On inflation, his net approval has crashed from +6 to -44.

If you own stocks, the 28% gain during the last year is a welcome cushion against rising costs and other economic stressors. But many Americans lack economic shock absorbers, which explains the very sour public mood.

You can order this cartoon ☝️ or others like it, plus merch featuring cartoons, at CartoonStock.com.

Love the cartoon 😂

I got a article today that offered me 10,000 dollars of life insurance for 137 dollars a month.Of course that was based on my age.Now i my case i still have a old insurance policy that is still active for 1,150 thousand dollars fro 116 dollars a month. Now in my case if i had to invest money right now i would just take my 137 and, buy me some silver dollars because i do not trust our government.God Bless !