Chartpack: The economic toll of the Iran war

A shaky ceasefire hasn't brought down energy prices, and the damage is spreading way beyond energy.

This is an updated version of a story first published on April 6.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~

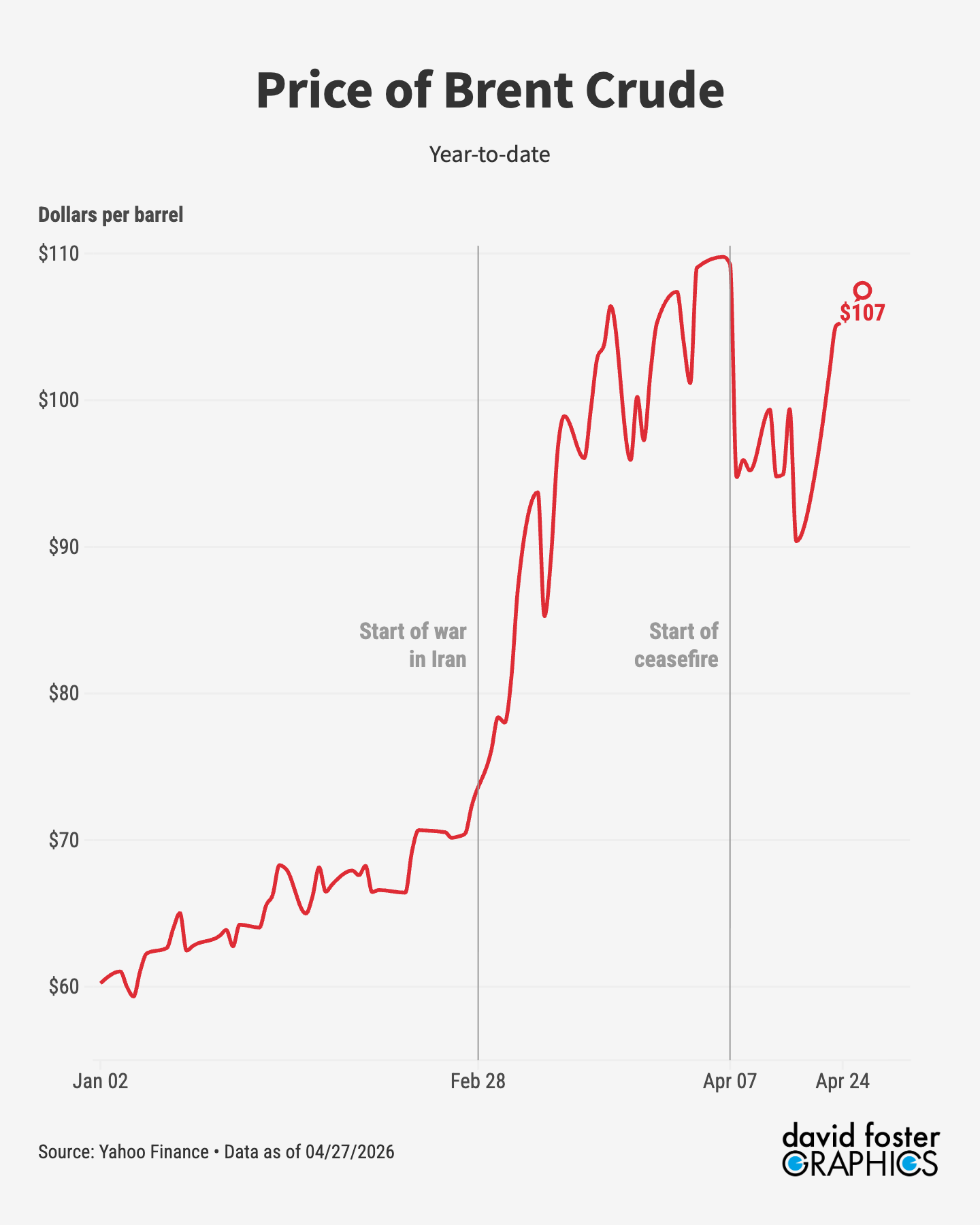

As everybody knows, the war President Trump launched against Iran on February 28 has caused a global energy crunch. Iran has stopped the flow of most cargo ships through the Strait of Hormuz, at the mouth of the Persian Gulf, while the US Navy is blocking some of Iran’s own oil exports. Investors think the war will end at some point this year, but Brent crude prices have still jumped from about $68 per barrel before the war to nearly $110 per barrel.

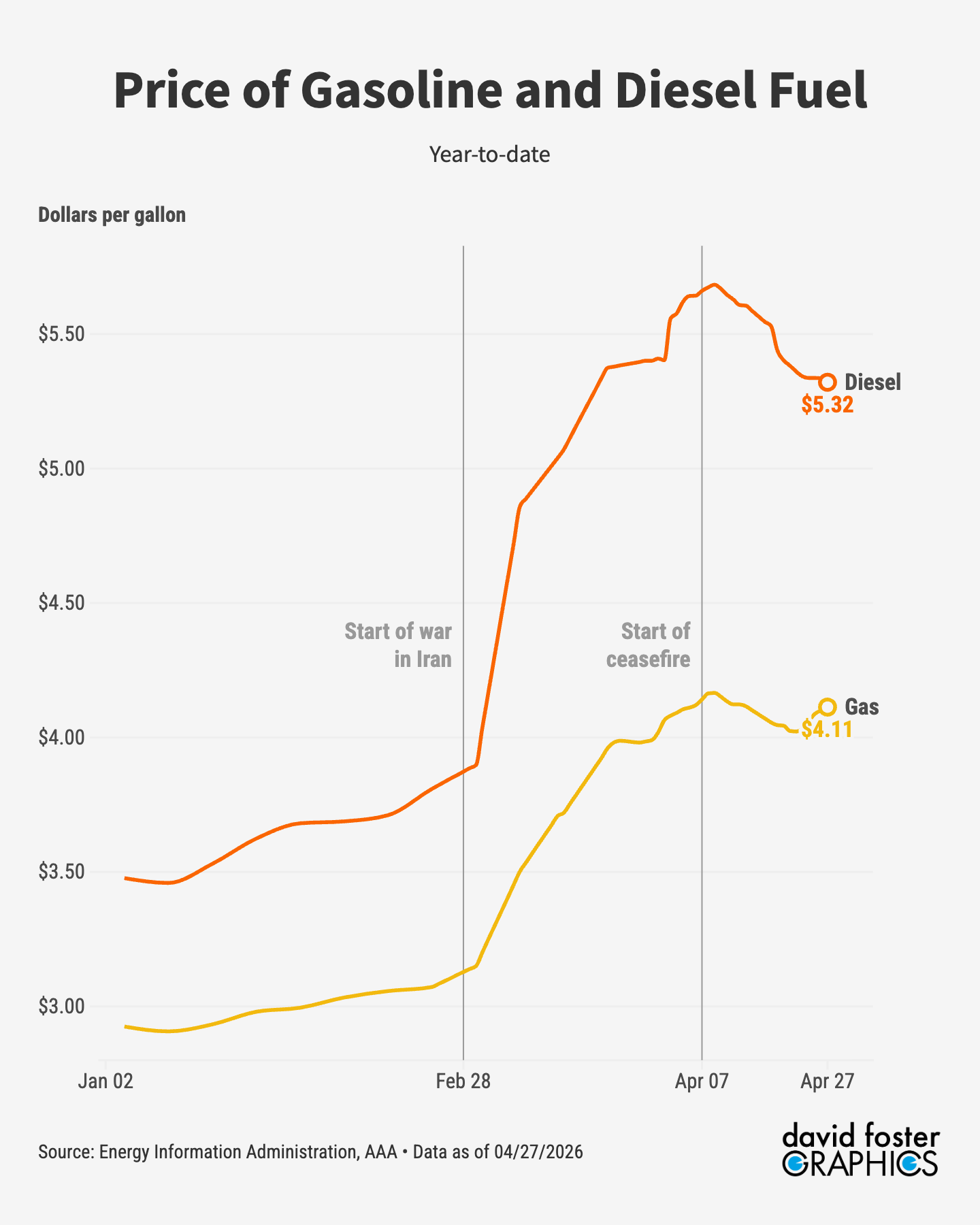

Gas prices have risen by more than $1 per gallon since the war started, to a national average of about $4.11. Diesel prices have risen by more, to about $5.32 per gallon. If oil prices stay above $100, gas and diesel prices will stay where they are and maybe go higher. A $1 jump in gas prices costs a typical driver about $40 a month in higher costs. If that lasts for the rest of the year, it will completely negate the larger tax returns many Americans received this year, on account of the 2025 tax-cut law.

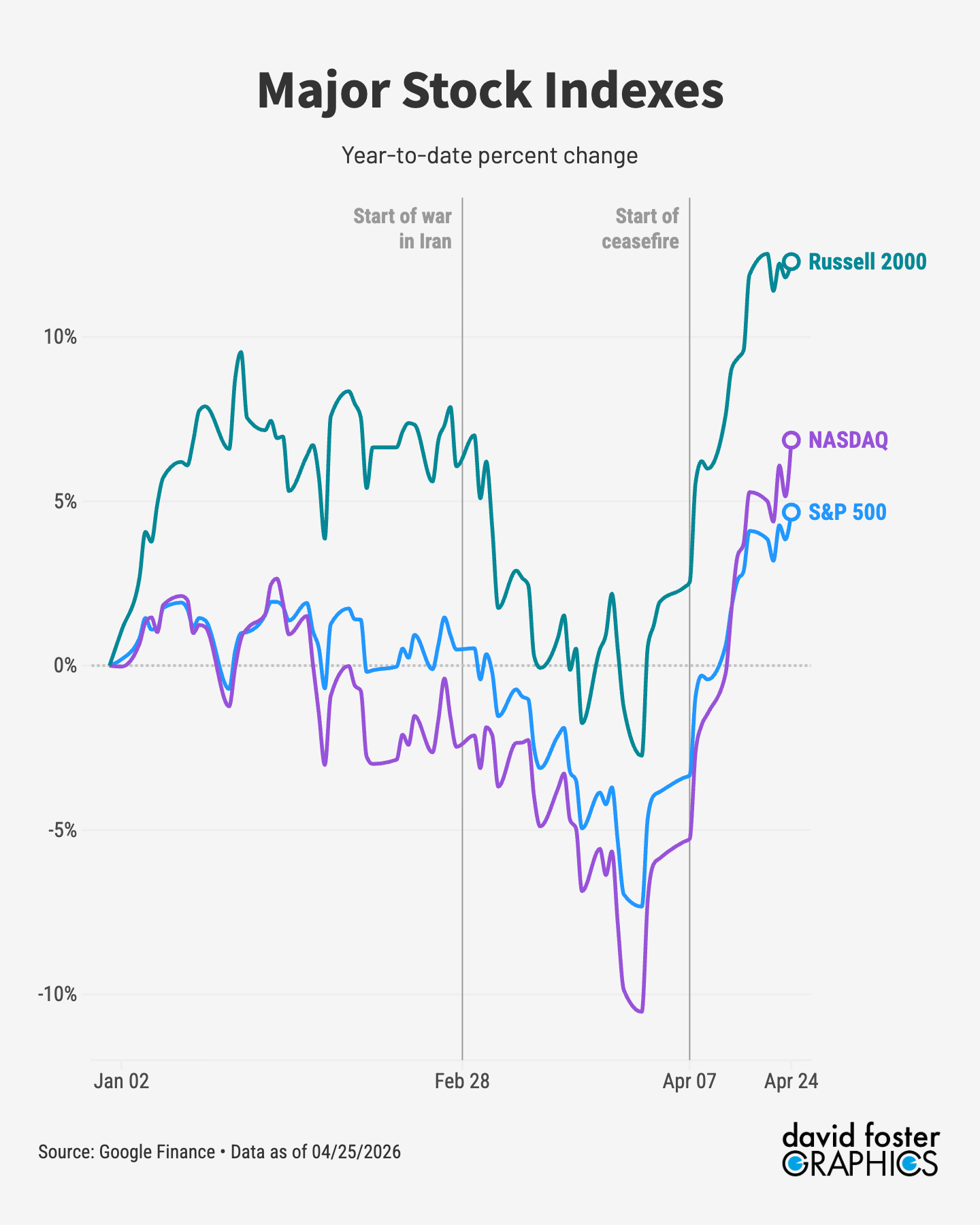

Stocks plunged during the first month of the war, but they’ve since recovered and are positive for the year. The artificial-intelligence revolution is going gangbusters regardless of the war, and investors see big gains in the future. That’s why stocks are rising. But it stands to reason that stocks would be higher still without the war.

[More: Why stocks are rallying, despite the war]

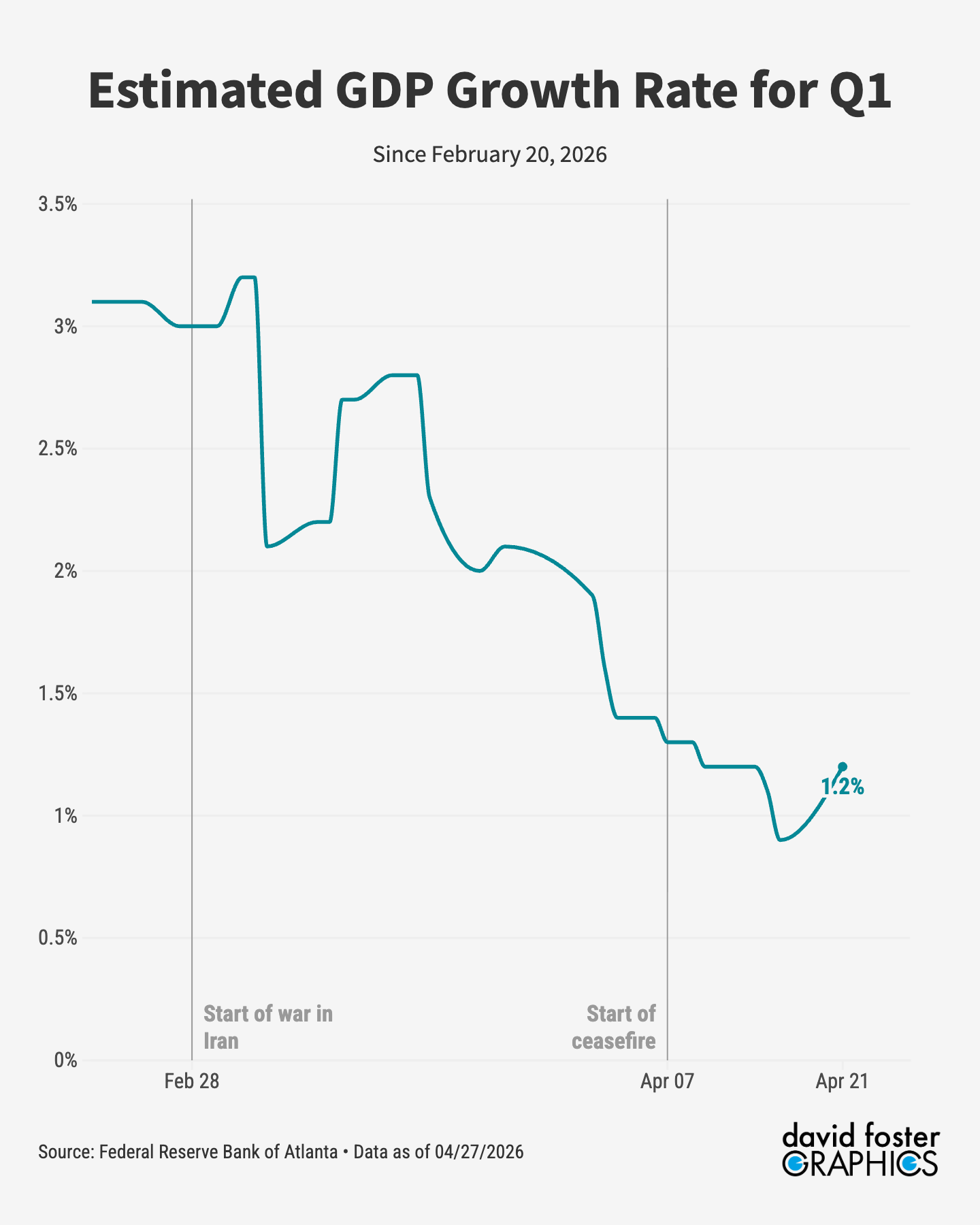

GDP growth will probably end up significantly lower because of the war. In late February, right before the war began, the Atlanta Federal Reserve’s GDP Now model estimated that first-quarter GDP growth was 3.1%. The estimate has since fallen to just 1.2% growth in the first quarter. Some of that might be delayed spending or investment that will take place later in the year. But some of that lower growth comes from canceled spending that won’t get made up.

Inflation will go higher than it would have without the war. The spike in energy costs makes it more expensive to produce and transport almost every type of good. The war also disrupted shipments of many industrial chemicals from the Gulf region, causing soaring prices for products such as fertilizer. That will also raise costs throughout the supply chain, all the way to consumers.

[Check out the Weekly WTF, stuff you can hardly believe]

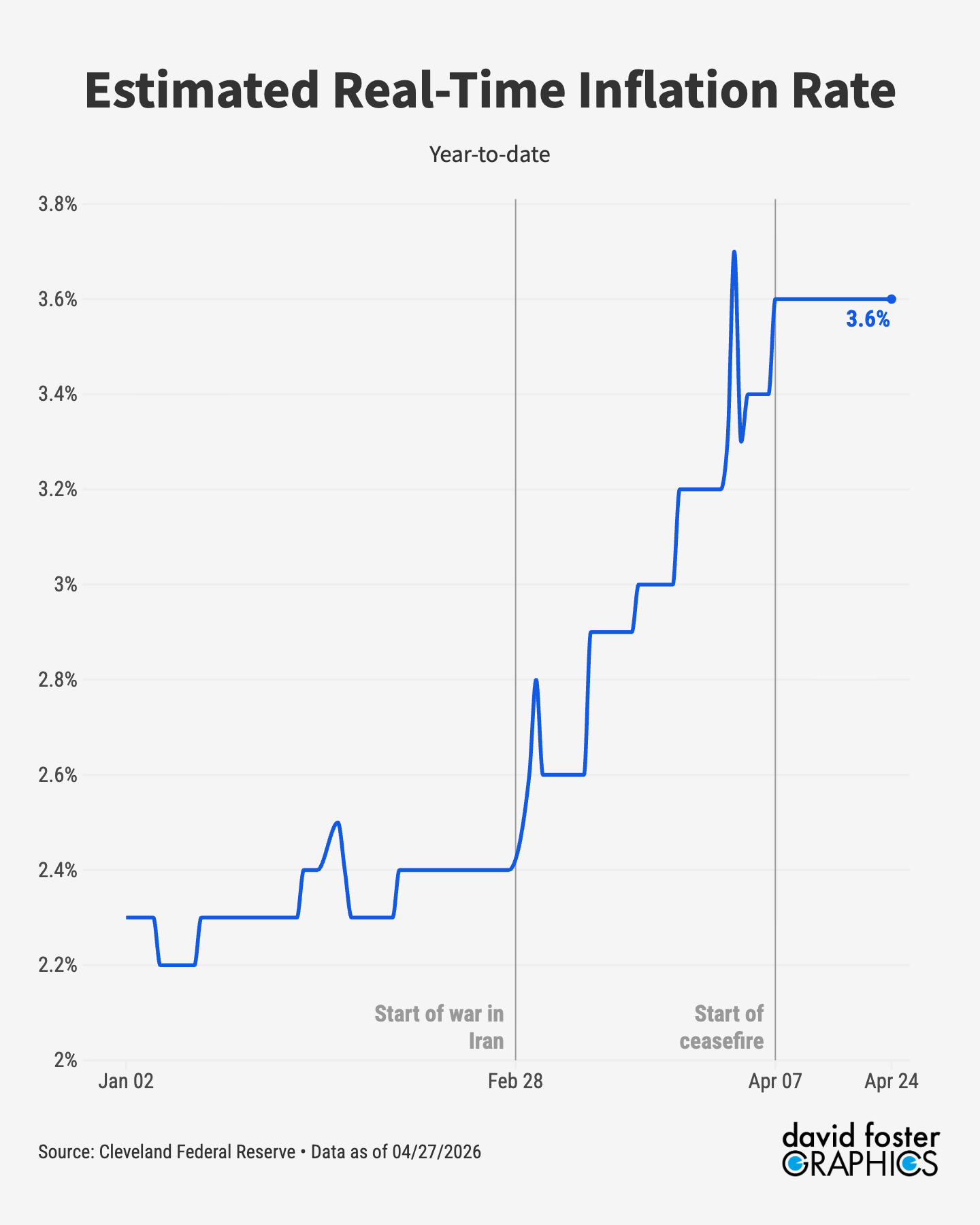

Before the war, the Cleveland Federal Reserve’s inflation “nowcast” was 2.4%. That’s an estimate of the real-time inflation rate, rather than the dated, backward-looking number that comes out monthly in official price reports. The inflation nowcast has since jumped to 3.6%, more than a point higher.

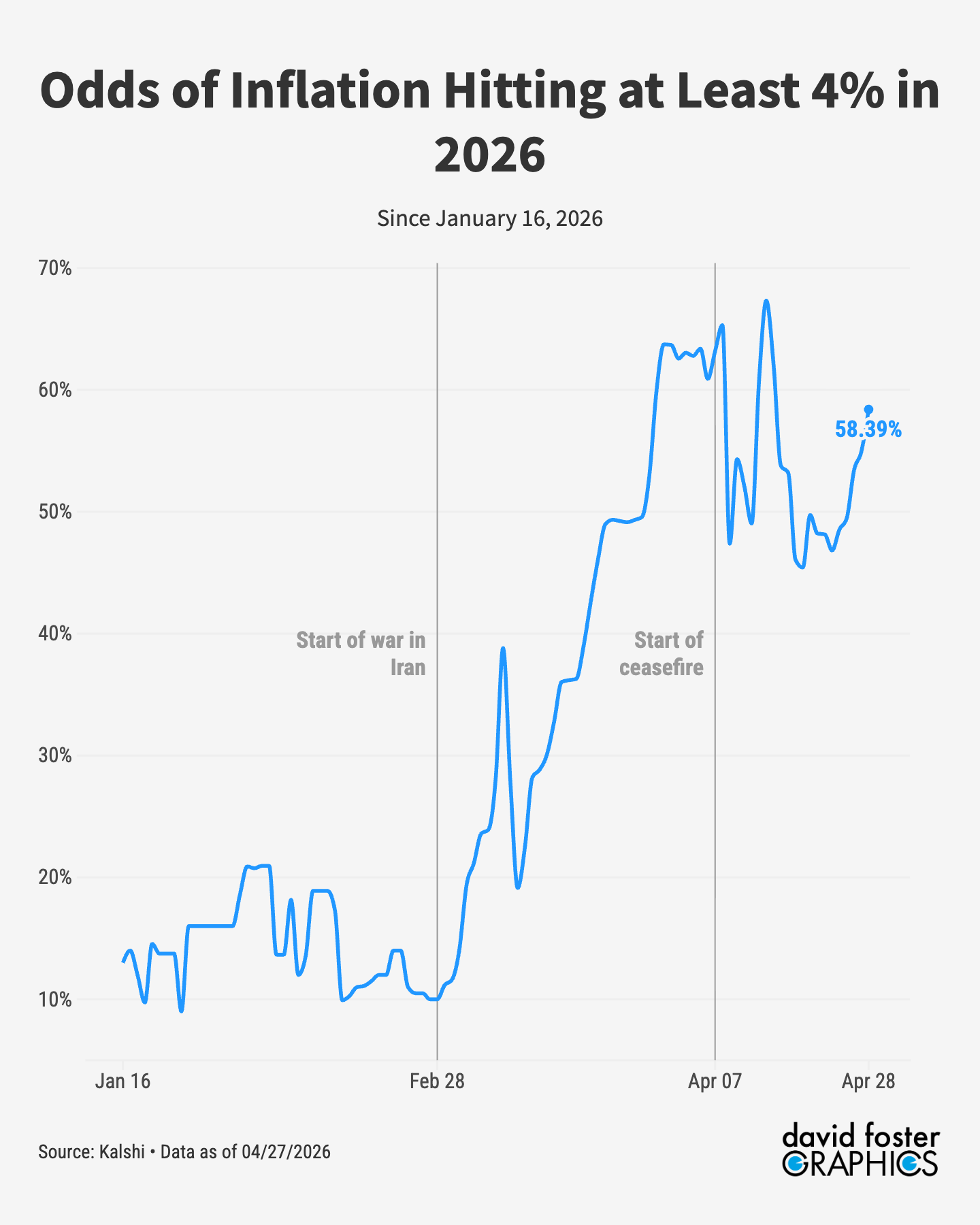

On the prediction market Kalshi, the odds of inflation hitting at least 4% in 2026 have jumped from just 10% before the war to 58% now.

Higher inflation usually means higher interest rates, because investors buying bonds demand a higher return to compensate for the eroding value of money. And sure enough, rates have marched upward right along with rising inflation expectations.

[See why it could take months for the Iran war to “end”]

The average 30-year mortgage rate has jumped from about 6% before the war to nearly 6.23%. That’s enough to raise the monthly payment on a typical home by about $50.

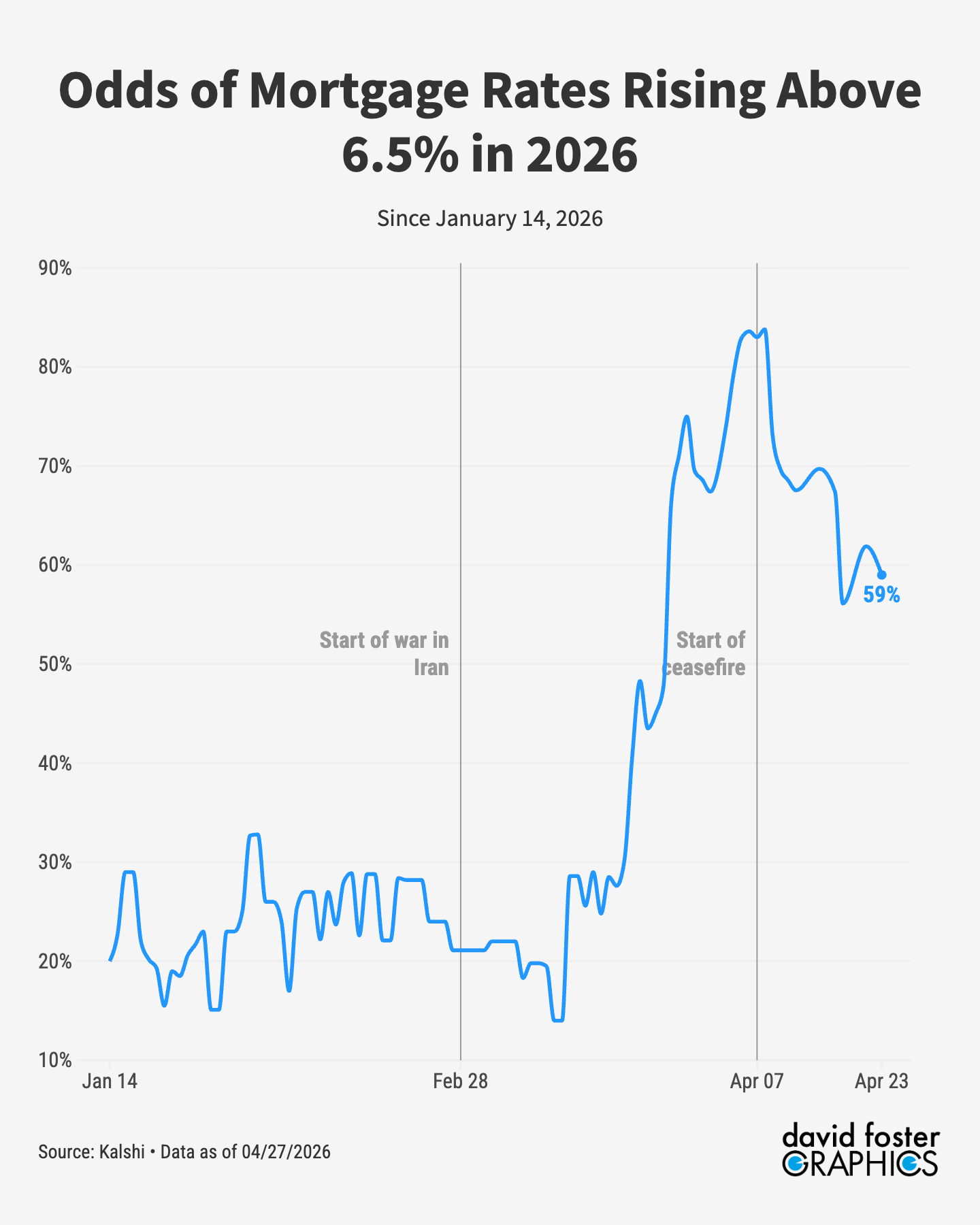

The outlook for interest rates is upward. Before the war, the odds of mortgage rates rising above 6.5% this year were just 21%, according to Kalshi. Now the odds of rates above 6.5% are 59%. Rates on most other loans will rise by about the same amount as mortgage rates.

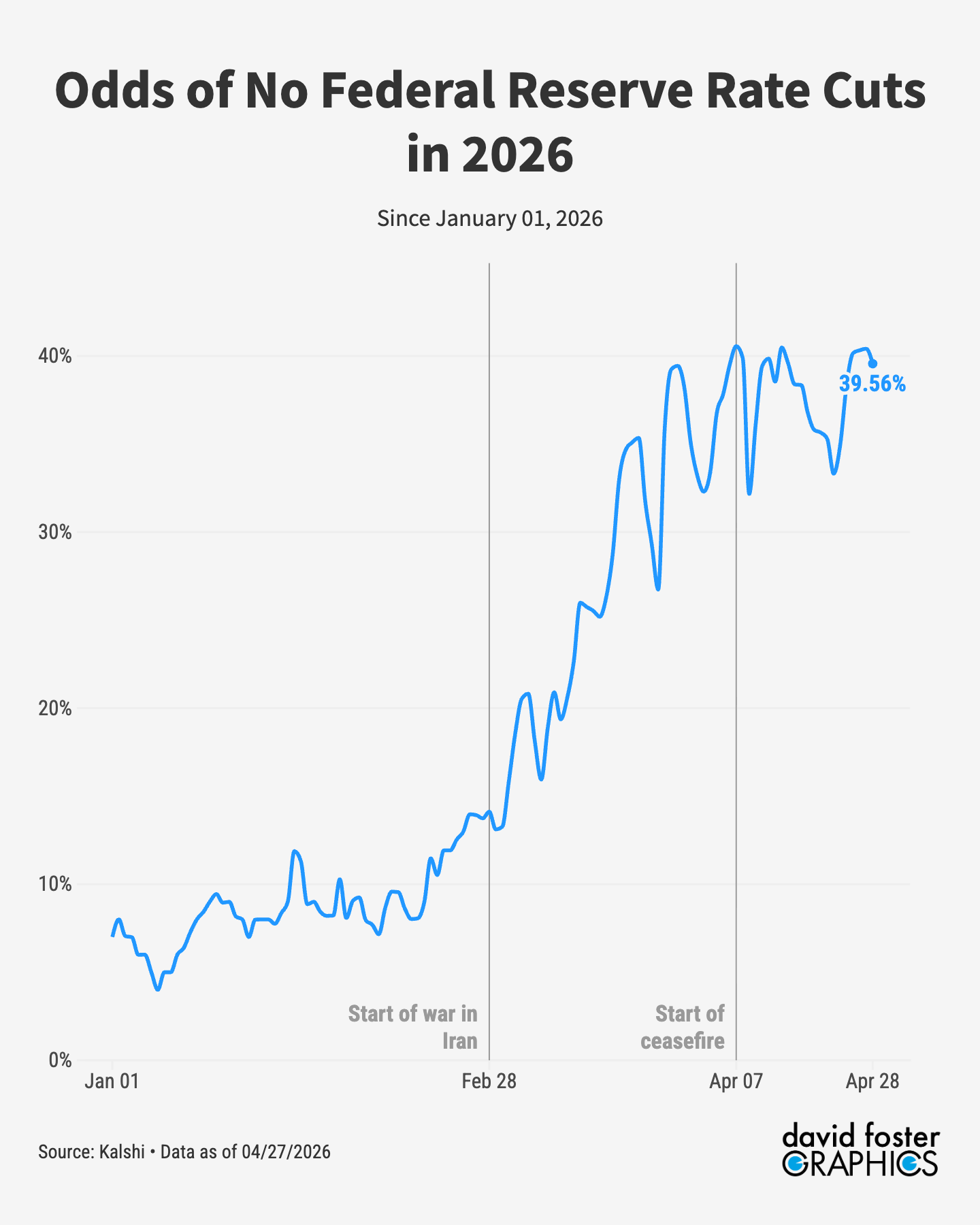

Will the Federal Reserve cut interest rates? Before the war, prediction markets put the odds of Fed rate cuts this year at 86%. But the Fed rarely cuts rates when inflation is rising, and the war-related surge of inflation has lowered rate-cut odds to 60%. This chart shows the odds of no rate cuts in 2026, surging from 14% in February to 40% now.

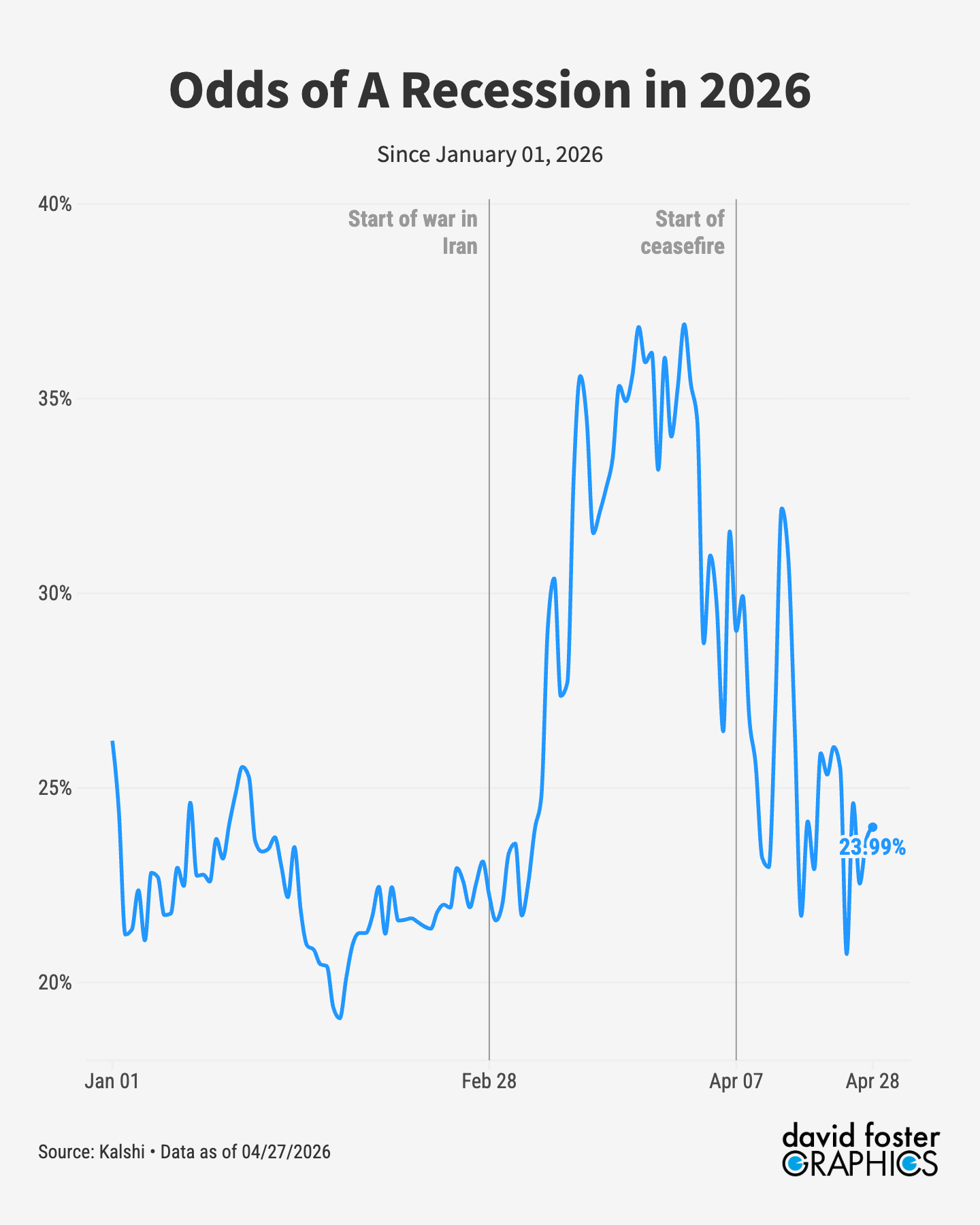

The good news, if you can call it that, is that economists still don’t think the war will cause a recession.

But high levels of uncertainty will remain as the world watches to see whether Iran is able to exploit what appears to be newfound leverage over Persian Gulf energy exports. The uncertainty alone will be destabilizing, possibly for a long time.

The charts are great. Thanks.

Good update, thanks!

(Just FYI - noticed that the graph with the odds of no rate cut in 2026 vs time during 2026 is included twice in the last section.)