Iran mars a solid inflation report

The Islamic Republic now gets a say on the level of US interest rates.

If President Trump hadn’t started the Iran war in February, the monthly inflation report would be a yawner and markets would be focused on other things. Yet inflation remains a problem and even good news comes with big asterisks.

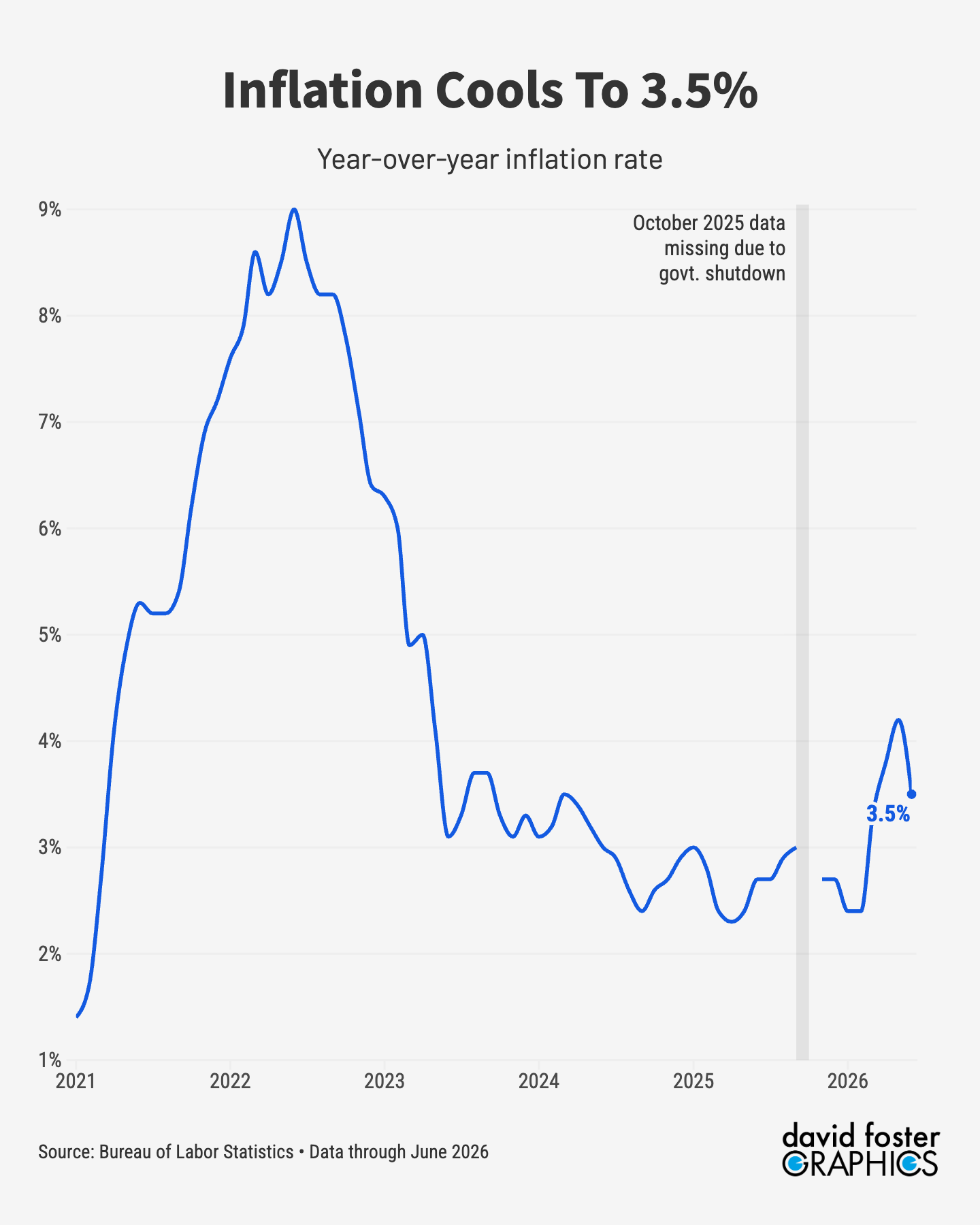

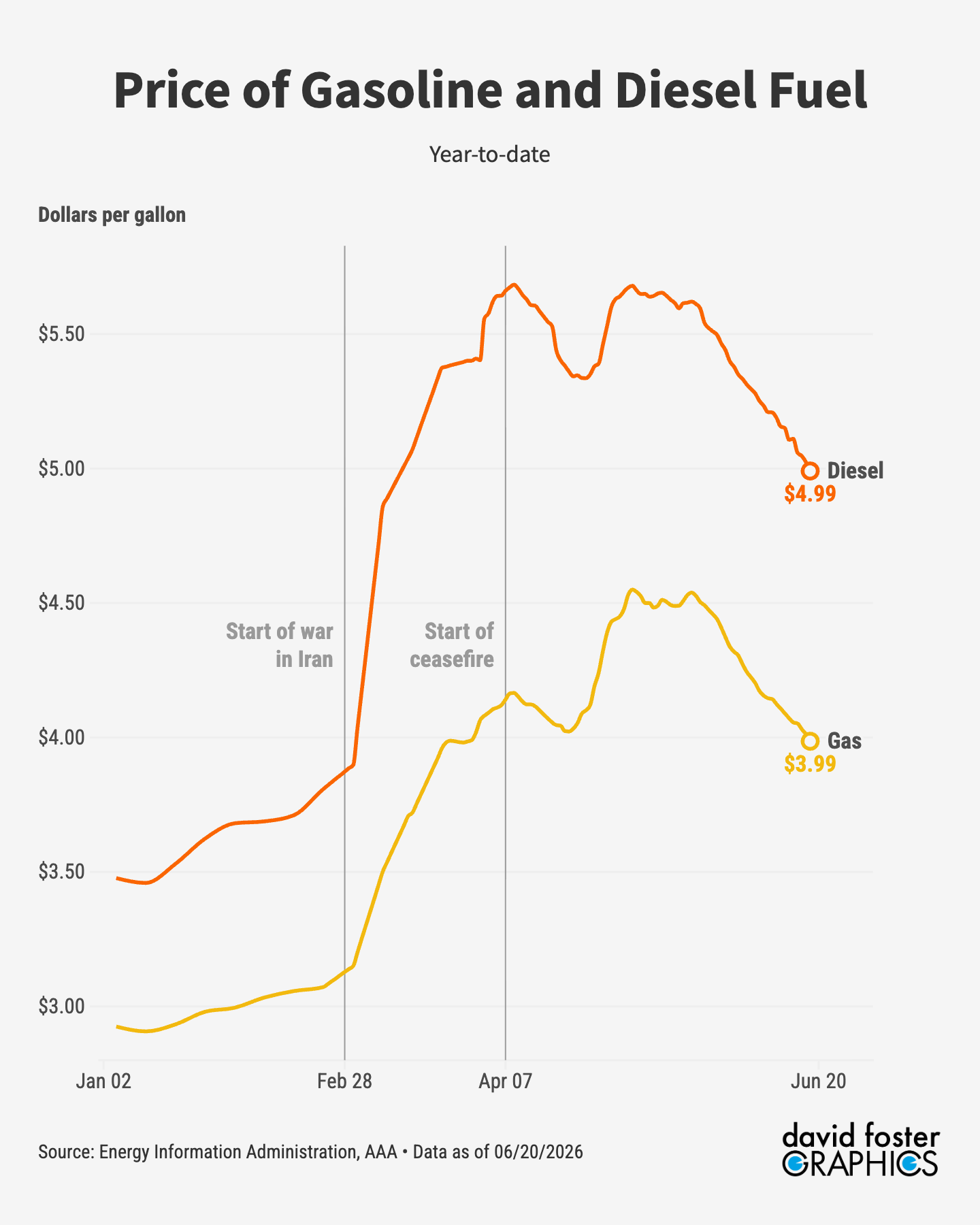

Inflation cooled in June, dropping to 3.5% from 4.2% in May. That’s obviously a welcome development. The biggest improvement was the huge drop in the price of oil and other commodities, as the Iran war simmered down and tanker traffic started moving through the Strait of Hormuz.

That’s almost irrelevant, however, given that the Iran war seems to be back on and oil prices are spiking again. So is inflation a problem, or not?

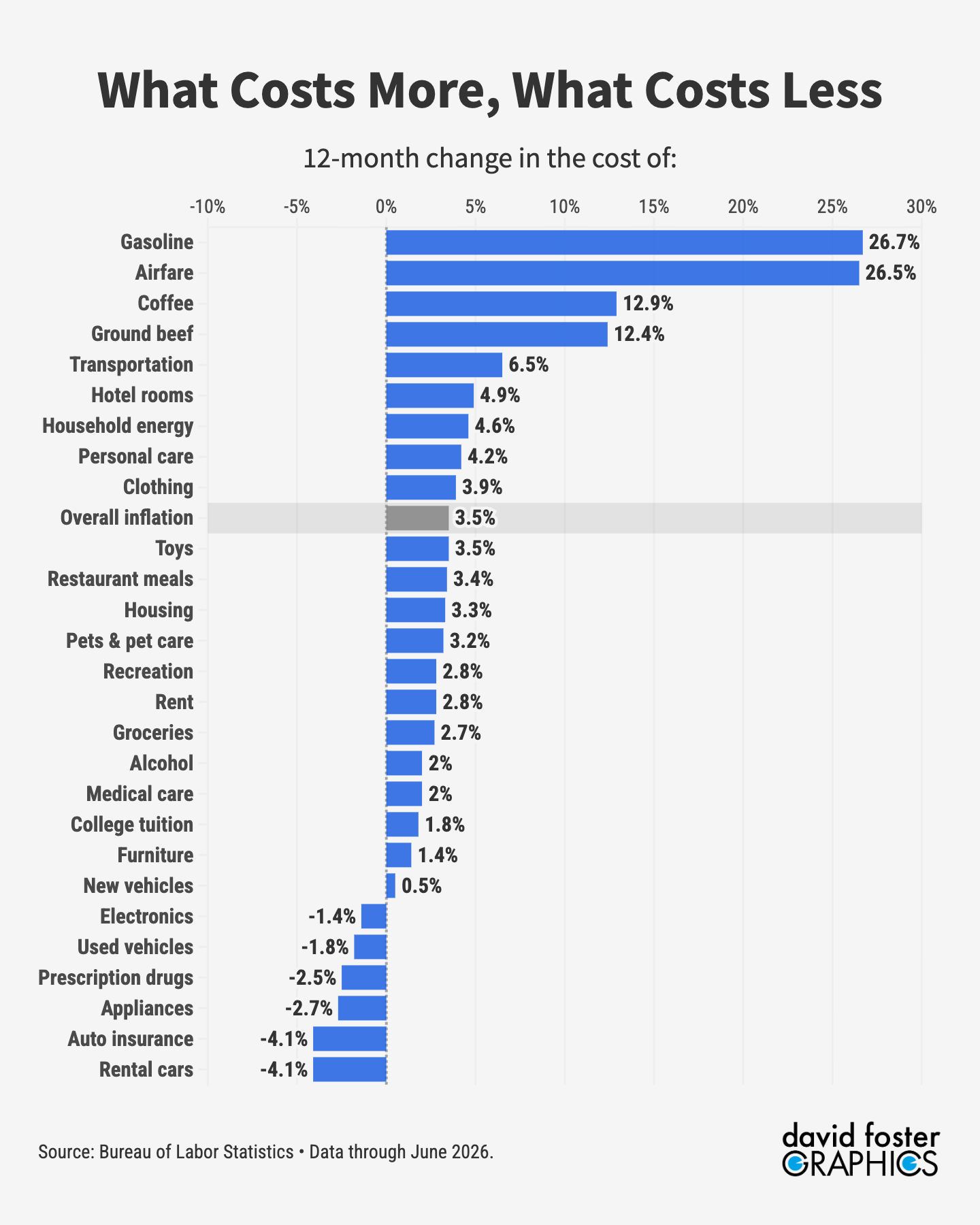

Both, alas. We track inflation every month in more than two dozen major categories, to isolate where the pain is. Here’s the breakdown:

Gasoline and airfares are up double-digits year-over-year entirely because of the Iran war. But those eye-popping numbers are better than they were last month. Annualized gasoline inflation, for instance, dropped from 40.5% in May to 26.7% in June.

[Check out The Matterboard: News that’s worth your time]

Ground beef and coffee prices are high mainly because of shortages. But those prices are gradually moderating. Grocery prices overall are up by a modest 2.7%. That would probably be lower without the war, because diesel is a big part of producing and transporting food, and the war drove diesel prices up.

Car prices, both new and used, are flat, after several years of runups. And car insurance costs are declining, after rising by double digits for a couple of years.

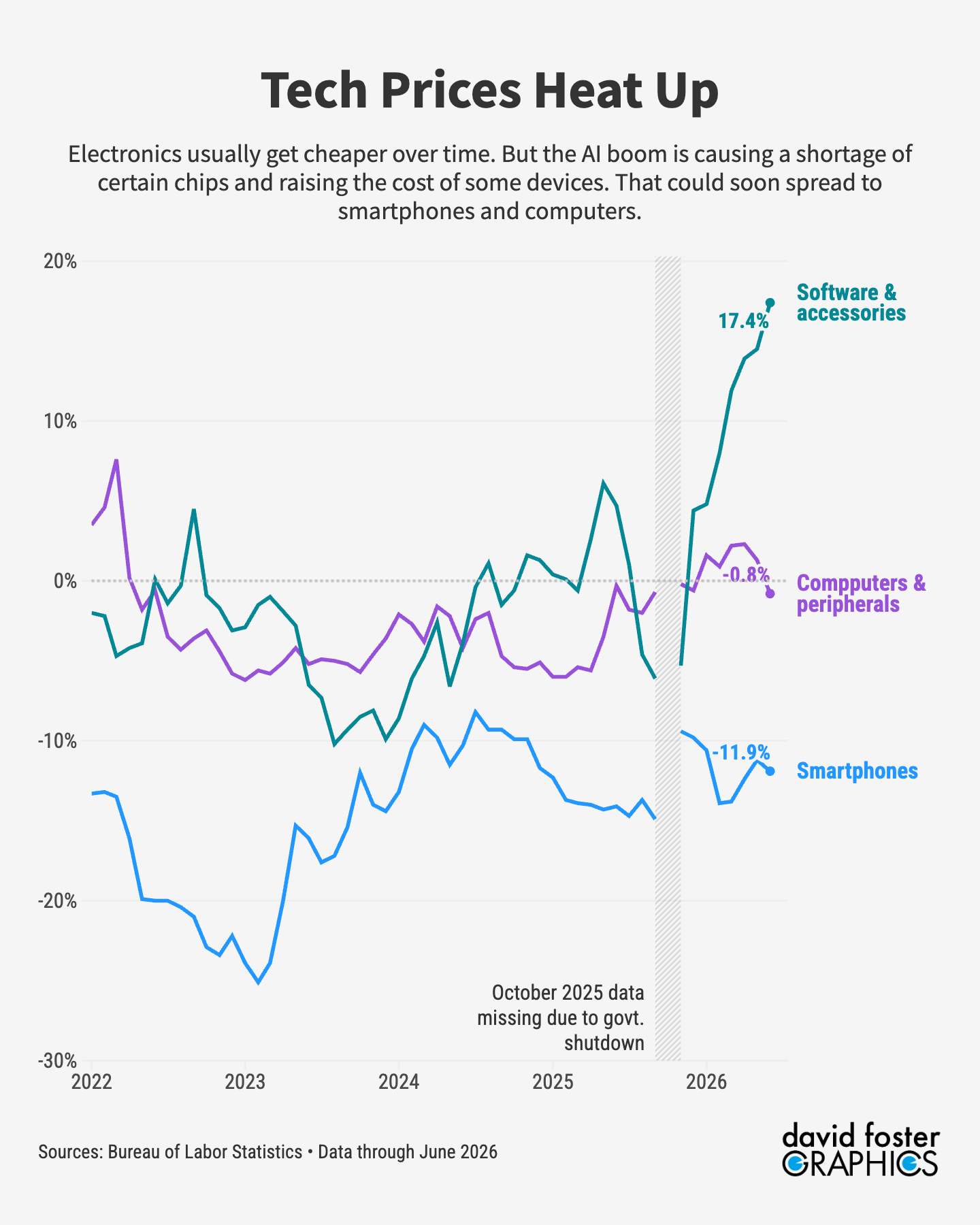

One new source of inflation in recent months has been electronics, due to the artificial intelligence boom and relentless demand for semiconductors. That has sent prices of those components soaring.

But the few categories where there’s sustained inflation represent a very small portion of consumer spending. The bottom line is that if you take war-related inflation out of the picture, there’s not much to worry about.

[The Weekly WTF: Trump out-gaffes Biden]

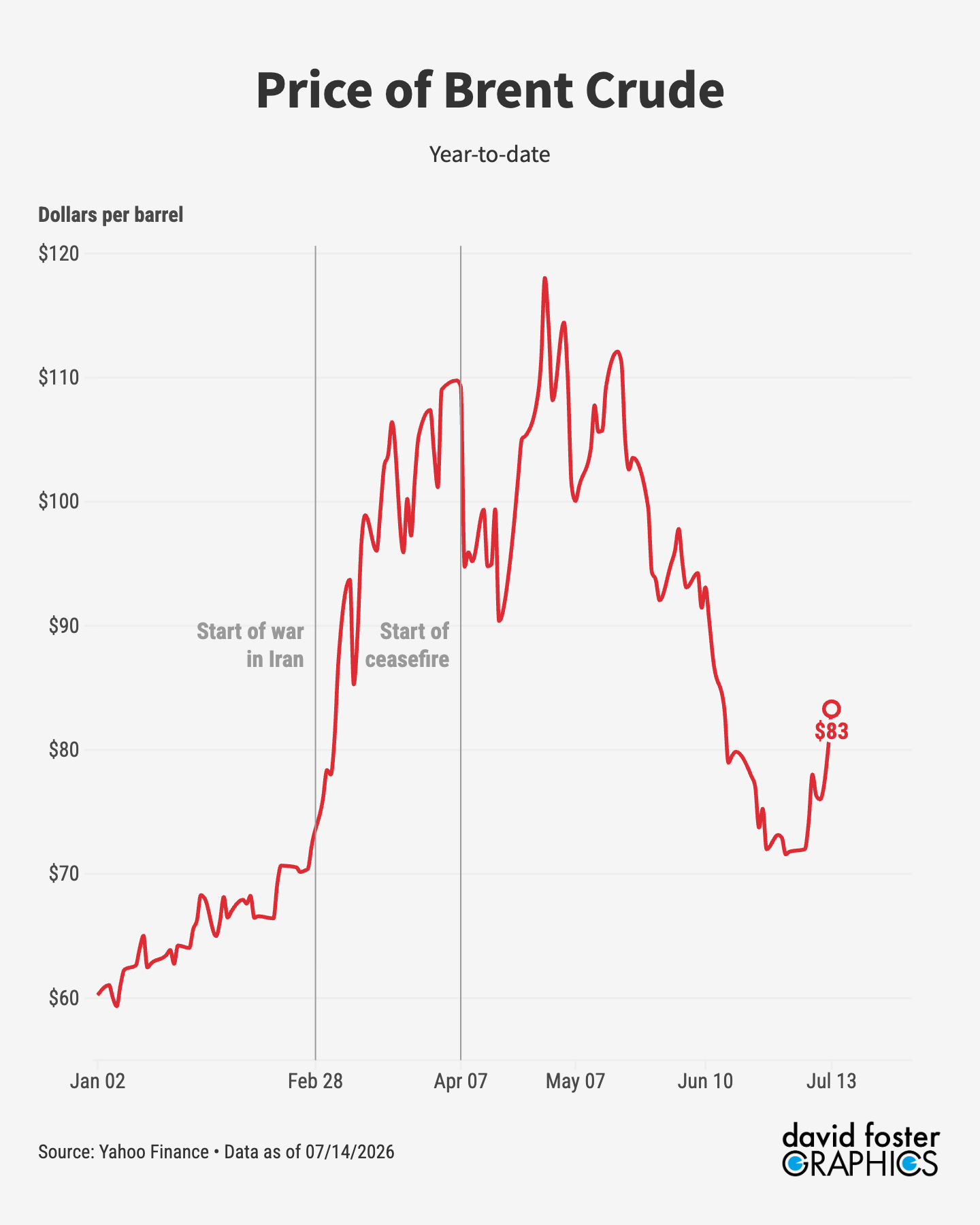

Obviously you can’t just pretend the war isn’t there, especially since everybody knows it will probably push the July inflation number higher. The US-Iran ceasefire has broken down, Iran is shooting at tankers periodically, and Trump says the US is reimposing its blockade of Iranian ports.

Oil prices were almost back to pre-war levels at the beginning of July, but they’ve now jumped by about $12 per barrel, to around $83. Gasoline prices will follow oil prices back up, as they always do.

Trump is in a bind because consumers hate inflation and his war has eroded purchasing power. Iran’s leaders knows this, and could keep the war going through the midterm elections in November—their way of punishing Trump and his fellow Republicans, even if more bombs rain down on them.

The inflation spike earlier this year turned real incomes negative, which means inflation was rising faster than wage gains, on average. The June inflation dip has brought both wage growth and inflation to 3.5%. So real wage growth is 0, which is better than a negative number. But that will probably turn negative again in the July data, assuming the inflation rate ticks back up.

The details matter for markets because they affect what the Federal Reserve might do. New Fed chair Kevin Warsh told Congress on July 14 that the central bank has “a resolute commitment to restoring price stability.” That’s Fedspeak for “we will do whatever is necessary to get inflation down.” Normally, that means the Fed will raise interest rates, which is the principal way of cooling the economy, easing demand, and bringing prices down.

But Iran is the wrench in the machine. If the war settles down for good, there might not be much inflation to worry about. And if the war escalates, surging oil prices might drive prices higher no matter what the Fed does.

[Trump mimics the socialist Mamdani]

The Fed’s next rate-setting meeting is at the end of July. The likelihood of a rate hike then is only around 12%, according to the CME’s Fedwatch tool. But markets still think the Fed will hike at some point this year, by one-quarter or one-half a point. That means the outlook in general is for higher inflation.

We’ve pointed out that some economists see a weak economy more in need of rate cuts, as a form of stimulus, than rate hikes to battle war-related inflation. But the Fed is very unlikely to cut rates as long as Hormuz-related pressures are on, and Iran could keep making trouble for months. The fog of war often extends far from the battlefield.

Enjoy a cartoon.

You can order this cartoon👆 and play cartoon-themed puzzles and word games at CartoonStock.com.