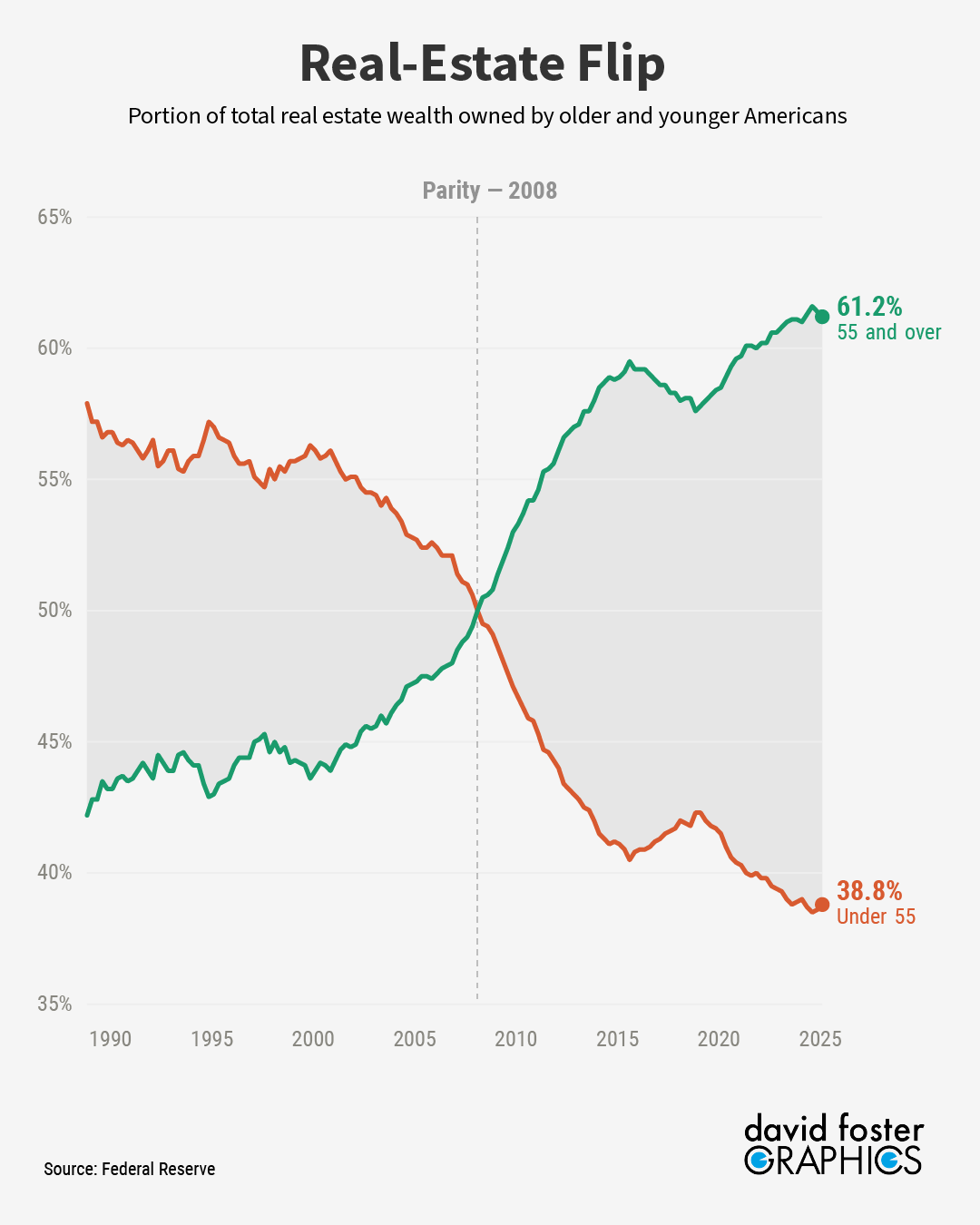

How older homeowners have locked up the housing market, in one startling chart

Younger Americans used to own most housing wealth in America. Not anymore.

Worsening wealth inequality has become a defining element of the US economy. The changes have mostly been incremental, with small year-to-year changes gradually funneling more and more of the nation’s riches to the wealthiest Americans.

But one change has been stark: The shift of real-estate assets away from younger Americans, toward older ones. And this helps explain the ongoing affordability crisis, along with many Americans’ persistently negative views on the economy.

Graphic artist David Foster and I set out to map the changes in wealth during the last 40 years, using data from the Federal Reserve. Most of the trendlines changed bit-by-bit. You can see David’s interactive graphic here.

But when we split real-estate wealth into two age groups, representing older and younger Americans, the changes were more dramatic. The portion of real-estate wealth owned by younger Americans has been plummeting:

A wannabe home buyer might look at this chart and say, I coulda told ya that. It has become notoriously difficult for many working Americans to muster the money for a down payment and crack into homeownership. Home affordability hit the worst levels on record following the Covid pandemic in the early 2020s, when super-low interest rates led to a surge of buying that pushed prices through the roof. Affordability is still poor.

[More: Nobody’s fixing anything]

But the sharp drop in the portion of real-estate wealth owned by Americans under 55 has been underway for a quarter century. Some of it comes from an aging society. Americans 55 and older represent 30.1% of the population today, up from 20.6% in 1989, when the Fed’s wealth data series begins. Those under 55 have dropped from 79.4% of the population to 69.9%. Since older Americans represent a larger share of the population today, that alone should push their share of real-estate wealth higher.

But that still doesn’t explain the magnitude of the shift. The share of housing wealth owned by older Americans has jumped by nearly 20 percentage points, roughly double the gain in population share. The share owned by younger Americans has dropped by the same amount.

[More: The economic toll of the Iran war is spreading]

This is where some of the adverse trends of the last few decades factor in. Since 1980, home prices adjusted for inflation have jumped by 68%, while incomes have risen by just 10%. Builders focus on large homes they can sell for the most money, while tight zoning rules and other barriers limit the supply of cheaper starter homes.

The total amount of student loan debt has ballooned from $260 billion in 2004 to $1.7 trillion today, more than a sixfold increase. That has obviously saddled younger workers. The total student debt load held by 18-to-29-year-olds has more than doubled, from $140 billion to $300 billion. For thirtysomethings, the amount of student debt has jumped from $110 billion to $520 billion, nearly a fivefold increase. These payments make it even harder to save for the down payment on a house and to cover the mortgage once you make a purchase.

Housing wealth has grown by a lot since 1989, and every age group has benefited in raw terms. The total value of residential real estate has mushroomed from $7 trillion to $47.9 trillion since 1989 For those 55 and over, real estate wealth has grown by $26.4 trillion. For those under 55, it has grown by $14.6 trillion.

[More: Trump says to hell with affordability]

But notice how lopsided the gains have been. Older Americans who represent 30% of the population have captured 64% of the gain in home values since 1989. We see the same trend in declining homeownership rates for younger people. The homeownership rate for 35-to-44-year-olds, for instance, has dropped from 67% to 60% since 1990. That’s a lot of people who aren’t buying homes and benefiting from rising values over time, as prior generations did.

This could have a lot to do with why some Americans seem to think the US economy is permanently in recession. The University of Michigan’s sentiment index is at the lowest level in a series that dates to 1962. Yet the economic data is solid and there’s no recession, by standard measures. Overall spending is holding up, but that’s largely driven by wealthy Americans who have benefited from the soaring values of homes and stocks. On the bottom rung of the K-shaped economy, millions of Americans who feel like they can’t get ahead are perpetually gloomy.

The point isn’t that older Americans own too much real estate and ought to cough some of it up. A lot of that wealth will filter to younger generations eventually, through inheritances.

The problem is that younger Americans face too many barriers to homeownership and to building wealth during their prime earning years. There’s a bipartisan bill in Congress meant to provide federal incentives to break permitting logjams and take other steps to produce more housing. It would probably do some good, but it might not pass.

Housing is mostly regulated locally, and there are a lot of things states and cities can do to lower costs, such as cutting red tape, easing land-use laws and creating incentives for developers to build more multifamily housing.

Hopeful buyers have other choices. They can move from expensive coastal cities to more affordable ones in the Midwest or South. And living with parents to save money has become so common there are now guidelines for how to do it right. While you’re there, maybe drop a hint about getting an early inheritance.

Enjoy a cartoon.

You can order this cartoon ☝️ or others like it, plus merch featuring cartoons, at CartoonStock.com.

How much do you think the impact of the unindexed capital gain exclusion on the sale of a house plays a role (assuming you owned the house for five years and lived in it for at least two)? The exclusion has stayed at $500K for a couple (MFJ tax status) since it was set up in the late 90s. If they had indexed this figure to an annual inflation measure like so many other things in the tax code, might more “old”people who wish to downsize be tempted to sell their property to a younger family with kids and not have to worry about losing money to taxes?

In 2001, in tiny little neighborhood of Oakmont, we bought our house for $132,000. 25 years later, a comparable house across the street is on the market for $680K

Crazy

We have about 40 single family homes around town that’d be perfect starter homes.

4 families own them all and rent them out

One Funeral director made the switch after gobbling up properties w “insider” tips.

I guess it’s A way to get the heads up when homeowners are leaving their buffet first, I guess.

I assume The proliferation of rental properties hit after the 08 housing bust.