Here’s the economic toll of the Iran war (so far)

If the ceasefire lasts, it will limit the damage--yet many scars remain

The war with Iran that President Trump launched on February 28 might be over, if a shaky “ceasefire” Trump announced on April 7 holds. Markets certainly hope that’s the case. Oil prices tumbled in response to the ceasefire, and stock values jumped.

But we’re not going back to pre-war norms any time soon. Nearly six weeks of fighting caused massive disruption to energy markets and ground some economic activity to a halt. Some economic losses won’t be recovered. Other things will take weeks or months to return to pre-war levels. Some things may change permanently.

Here’s where we stand:

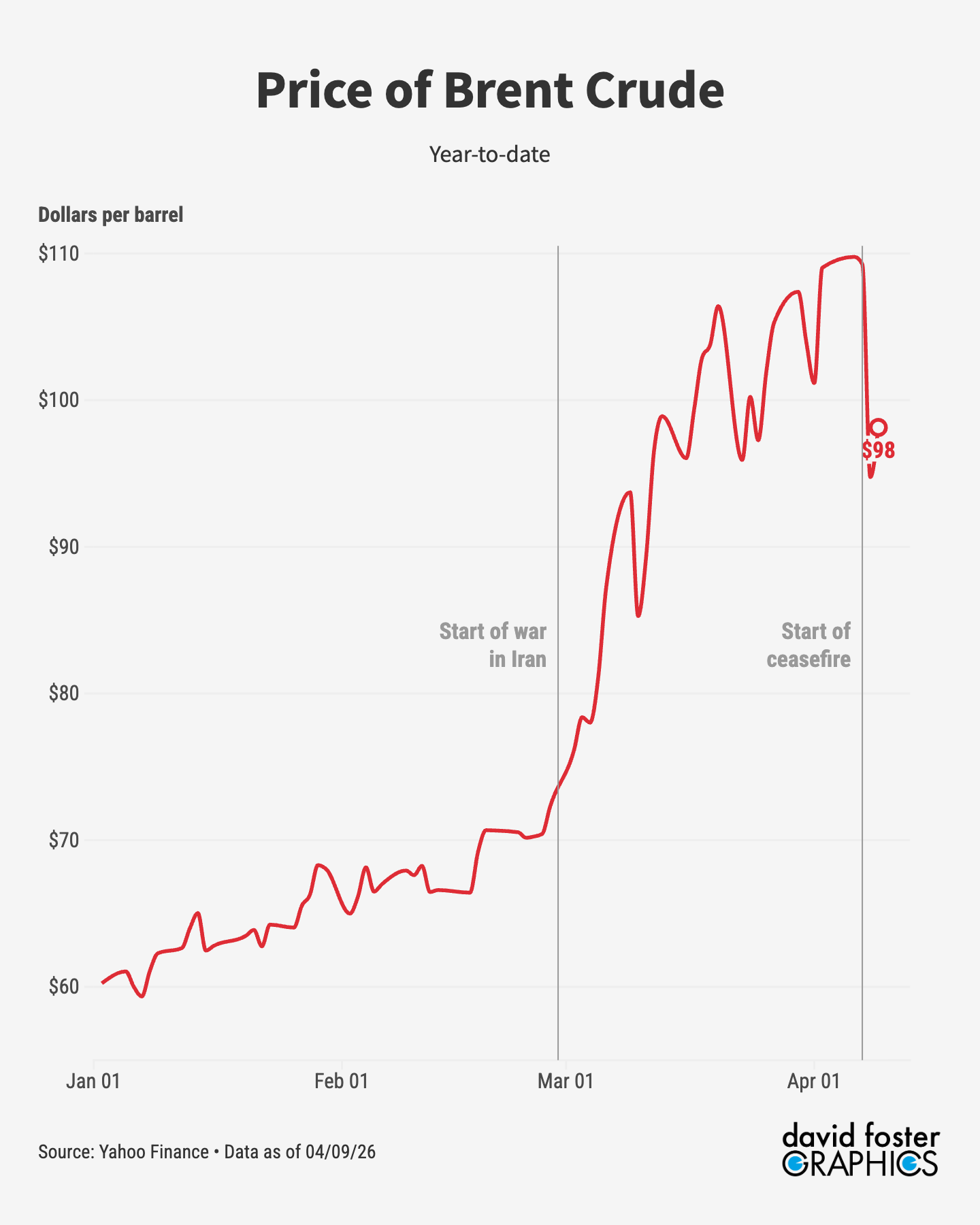

Oil prices fell from around $110 before the ceasefire to about $98 after. That triggered a robust stock rally on April 8. But oil prices are still 50% higher than they were before the war. And they may stay there for a while. While a ceasefire may set the stage for shipping to resume through the Strait of Hormuz, where 20% of the world’s oil exports must pass, conditions are different now.

Before the war, ships passed freely. Now Iran is exerting control over the strait, deciding who sails through and charging a “toll” of around $2 million per ship, or about $1 per barrel. Iran is also throttling traffic. In the first days after the ceasefire, tanker traffic through the strait was only about 10% of pre-war volume. Oil prices may stay near current levels for the indefinite future, especially if Iran’s new controls over the strait look to be permanent.

[See 5 huge problems with the Iran war ceasefire]

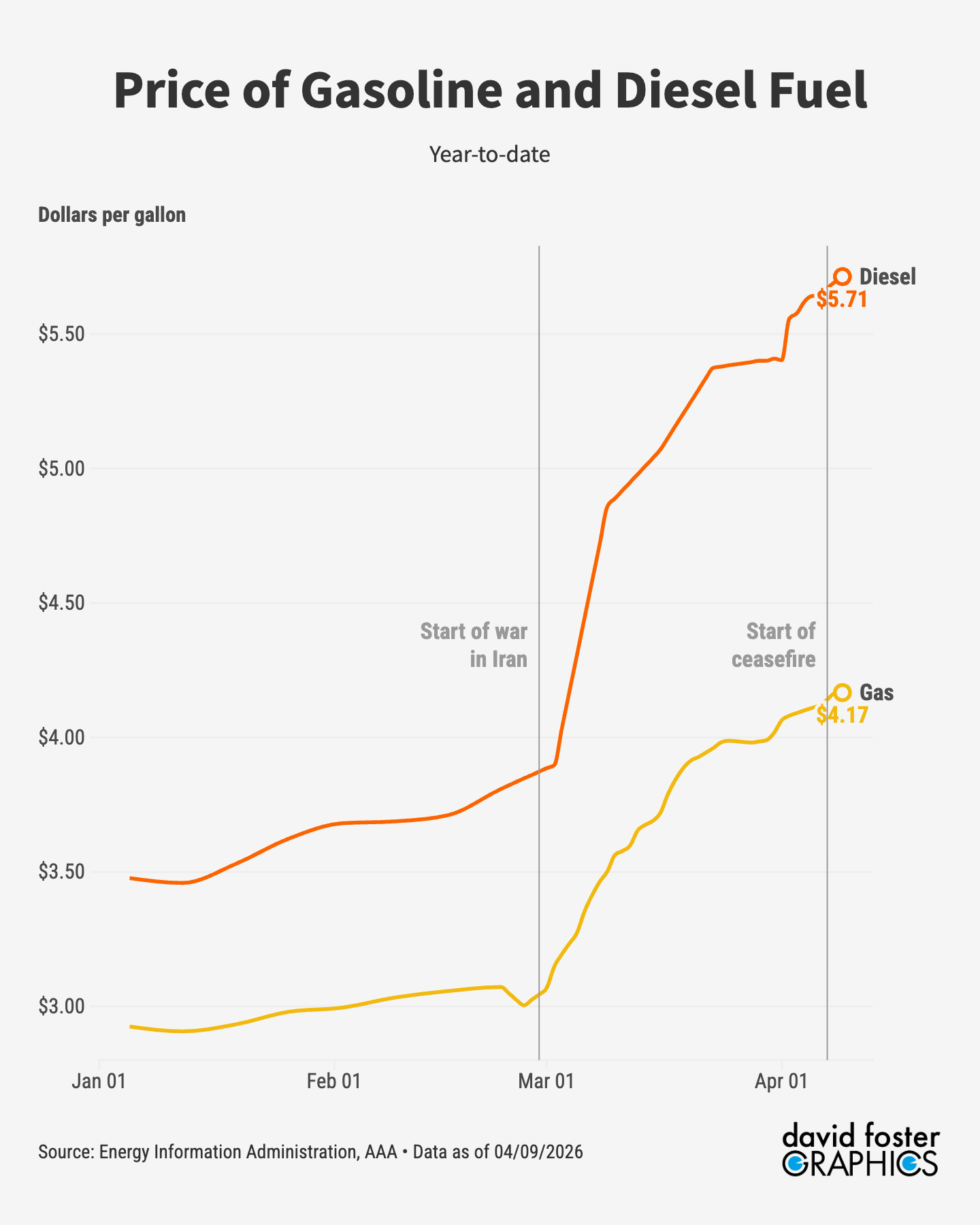

Gas prices have risen by about $1.20 per gallon since the war started, to a national average of about $4.17. Diesel prices have risen by more, to about $5.70 per gallon. If oil prices stay in the $90s, gas and diesel prices are unlikely to drop by much. A $1 jump in gas prices costs a typical driver about $40 a month in higher costs. The total hit to drivers from the jump in gas prices is $8 billion and rising.

Stocks enjoyed a strong rally after the ceasefire, but the S&P 500 index is still about 2% lower than pre-war levels. Trump bragged repeatedly when the Dow Jones index hit 50,000 for the first time on February 6. The Dow is now below 48,000.

GDP growth will probably end up lower because of the war. In late February, right before the war began, the Atlanta Federal Reserve’s GDP Now model estimated that first-quarter GDP growth was 3.1%. The estimate has since fallen to just 1.3% growth in the first quarter. Some of that might be delayed spending or investment that will take place later in the year. But some of that lower growth comes from canceled spending that won’t get made up.

Inflation will go higher than it would have without the war. The spike in energy costs makes it more expensive to produce and transport almost every type of good. The war also disrupted shipments of many industrial chemicals from the Gulf region, causing soaring prices for products such as fertilizer. That will also raise costs throughout the supply chain, all the way to consumers.

Before the war, the Cleveland Federal Reserve’s inflation “nowcast” was 2.4%. That’s an estimate of the real-time inflation rate, rather than the dated, backward-looking number that comes out monthly in official price reports. The inflation nowcast has since jumped to 3.4%, a full point higher.

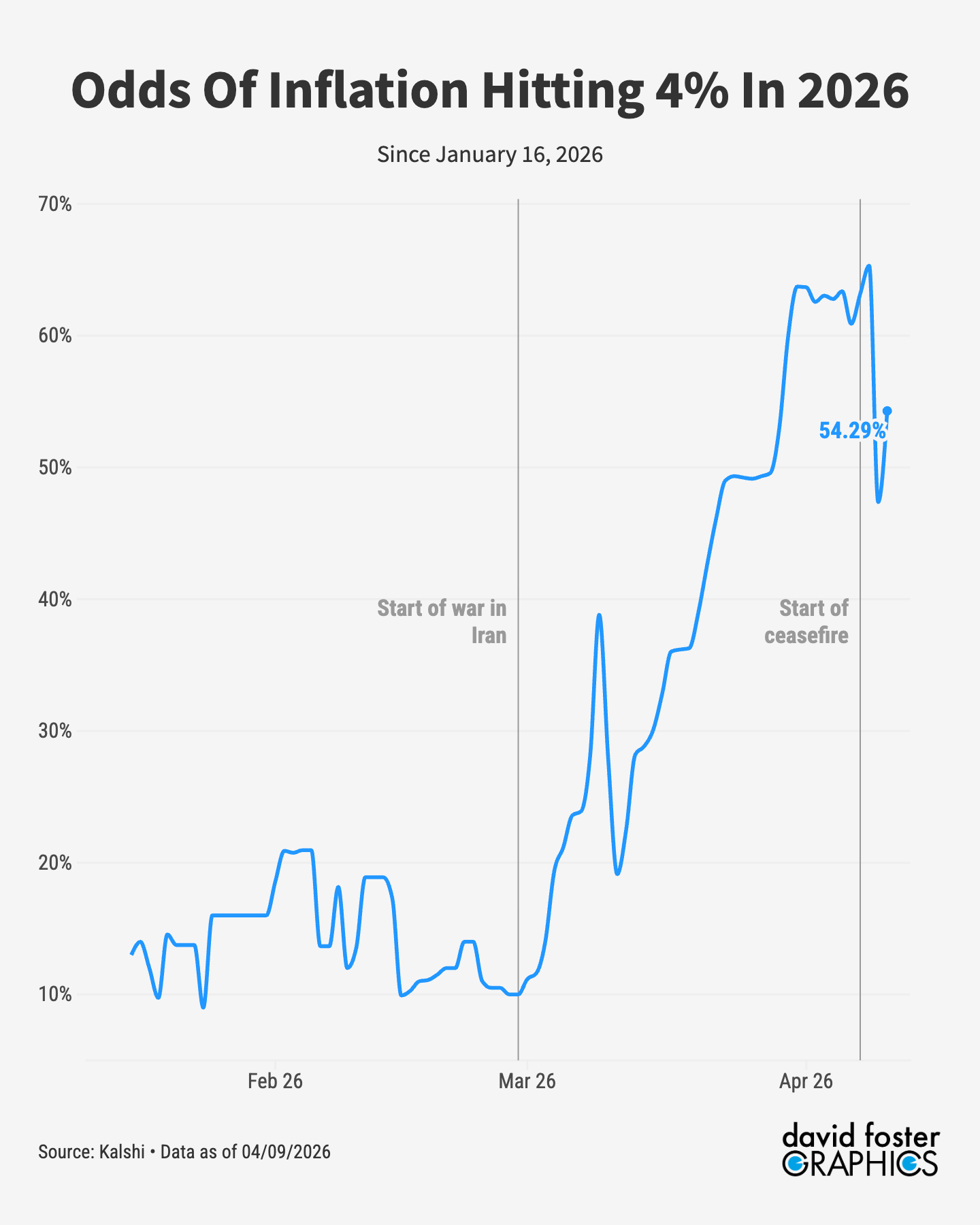

On the prediction market Kalshi, the odds of inflation hitting 4% in 2026 have jumped from just 10% before the war to 54% now.

Higher inflation usually means higher interest rates, because investors buying bonds demand a higher return to compensate for the eroding value of money. And sure enough, rates have marched upward right along with rising inflation expectations.

The average 30-year mortgage rate has jumped from about 6% before the war to nearly 6.4%. That’s enough to raise the monthly payment on a typical home by about $100.

The outlook for interest rates is upward. Before the war, the odds of mortgage rates rising above 6.5% this year was just 21%, according to Kalshi. Now the odds of rates above 6.5% are 73%. Rates on most other loans will rise by about the same amount as mortgage rates.

The ceasefire has led to slight improvements in the economic outlook. Inflation expectations have dipped slightly since April 7, for example. But high levels of uncertainty will remain as the world watches to see whether Iran is able to exploit what appears to be newfound leverage over Persian Gulf energy exports. The uncertainty alone will be destabilizing, possibly for a long time.

I no what FUBAR means does everyone no. The part i like is the Operation Epic.You guy's are the best reporter's i no.God Bless!

Excellent analysis!

I may have mentioned this before, but Paul Krugman has correctly called this Operation Epic FUBAR. 😂😂